Welcome to lrboost’s documentation!¶

lrboost is an scikit-learn compatible simple stacking protocol for prediction. Additional utilities for machine learning are also included!

Getting Started¶

LRBoostRegressor works in three steps.

- Fit a linear model to a target

y This is the primary model accesible via

lrboost.primary_model

- Fit a linear model to a target

- Fit a tree-based model to the residual (

y_pred - y) of the linear model This is the secondary model accesible via

lrboost.secondary_model

- Fit a tree-based model to the residual (

Combine the two predictions into a final prediction in the scale of the original target

LRBoostRegressor defaults to sklearn.linear_model.RidgeCV() and sklearn.ensemble.HistGradientBoostingRegressor() as the linear (primary) and non-linear (secondary) model respectively.

>>> from sklearn.datasets import load_diabetes

>>> from lrboost import LRBoostRegressor

>>> X, y = load_iris(return_X_y=True)

>>> lrb = LRBoostRegressor().fit(X, y)

>>> predictions = lrb.predict(X)

>>> detailed_predictions = lrb.predict(X, detail=True)

>>> print(lrb.primary_model.score(X, y)) #R2

>>> print(lrb.score(X, y)) #R2

>>> 0.512

>>> 0.933

The linear and non-linear models are both fit in the fit() method and used to then predict on any new data. Because lrboost is a very slightly modified scikit-learn class, you can hyperparameter tune the tree model as you would normally.

predict(X)returns an array-like of final predictions with an option forpredict(X, detail=True)predict_dist(X)provides probabilistic predictions associated withNGBoostorXGBoost-Distributionas the non-linear estimators.

Any sklearn compatible estimator can be used with lrboost, and you can unpack kwargs as needed.

>>> from sklearn.datasets import load_iris

>>> from sklearn.ensemble import RandomForestRegressor

>>> from lrboost import LRBoostRegressor

>>> X, y = load_iris(return_X_y=True)

>>> ridge_args = {"alphas": np.logspace(-4, 3, 10, endpoint=True),

"cv": 5}

>>> rf_args = {"n_estimators": 50,

"n_jobs": -1}

>>> lrb = LRBoostRegressor(primary_model=RidgeCV(**ridge_args), secondary_model=RandomForestRegressor(**rf_args))

>>> lrb = LRBoostRegressor.fit(X, y)

>>> predictions = lrb.predict(X)

lrboost is not going to magically provide improved error in all circumstances.

Situations with extrapolation outside of the training dataset might be particularly useful.

Hyperparamter Tuning¶

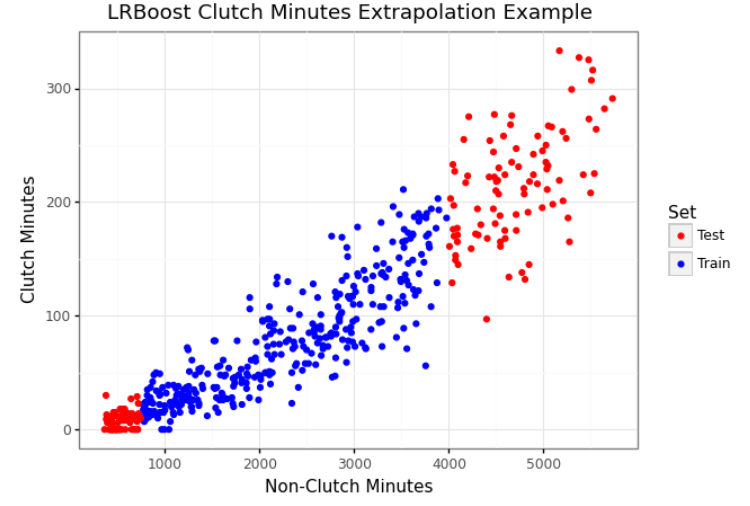

Model Comparison - Example 1¶

This is a (simplified) example of predicting clutch minutes from non-clutch minutes in NBA basketball.

It has a known linear and non-linear combination and extrapolation can be difficult.

Using the above test/train split we can show an extrapolation task on the tails of the distribution.

>>> import pandas as pd >>> import numpy as np >>> from sklearn.metrics import mean_squared_error >>> from sklearn.ensemble import HistGradientBoostingRegressor >>> clutch = pd.read_csv('../examples/clutch.csv') >>> train_mask = (clutch['nonclutch_min'] <= 4000) & (clutch['nonclutch_min'] >= 750) >>> train = clutch[train_mask] >>> test = clutch[~train_mask] >>> X_train = train[['nonclutch_min']] >>> y_train = train['clutch_min'] >>> X_test = test[['nonclutch_min']] >>> y_test = test['clutch_min'] >>> gbm = HistGradientBoostingRegressor(max_iter=500, random_state=42).fit(X_train, y_train) >>> lrb = LRBoostRegressor(secondary_model=HistGradientBoostingRegressor(max_iter=500, random_state=42)).fit(X_train, y_train) >>> print(f"Ridge RMSE: {round(mean_squared_error(lrb.primary_model.predict(X_test), y_test), 2)}") >>> print(f"HistGradientBoostingRegressor RMSE: {round(mean_squared_error(gbm.predict(X_test), y_test), 2)}") >>> print(f"lrboost RMSE: {round(mean_squared_error(lrb.predict(X_test), y_test), 2)}") >>> Ridge RMSE: 1385.81 >>> HistGradientBoostingRegressor RMSE: 3145.87 >>> lrboost RMSE: 1080.42

If we also attempt a general train/test split, lrboost performs well.

>>> Ridge RMSE: 570.01 >>> HistGradientBoostingRegressor RMSE: 743.66 >>> lrboost RMSE: 733.4

Model Comparison - Example 2¶

The following are some simple examples taken from Zhang et al. (2019)

>>> import pandas as pd >>> import numpy as np >>> from sklearn.metrics import mean_squared_error >>> from sklearn.ensemble import HistGradientBoostingRegressor >>> from sklearn.model_selection import train_test_split >>> concrete = pd.read_csv("../examples/concrete_data.csv") >>> features = ['cement', 'slag', 'fly_ash', 'water', 'superplastic', 'coarse_agg', 'fine_agg', 'age', 'cw_ratio'] >>> target = 'ccs' >>> def evaluate_models(X_train, X_test, y_train, y_test): >>> lrb = LRBoostRegressor(primary_model=RidgeCV(alphas=np.logspace(-4, 3, 10, endpoint=True))) >>> lrb.fit(X_train, y_train.ravel()) >>> detailed_predictions = lrb.predict(X_test, detail=True) >>> primary_predictions = detailed_predictions['primary_prediction'] >>> rb_predictions = detailed_predictions['final_prediction'] >>> hgb = HistGradientBoostingRegressor() >>> hgb.fit(X_train, y_train.ravel()) >>> hgb_predictions = hgb.predict(X_test) >>> print(f"Ridge RMSE: {round(mean_squared_error(primary_predictions, y_test.ravel()), 2)}") >>> print(f"HistGradientBoostingRegressor RMSE: {round(mean_squared_error(hgb_predictions, y_test.ravel()), 2)}") >>> print(f"lrboost RMSE: {round(mean_squared_error(lrb_predictions, y_test.ravel()), 2)}")

>>> # Scenario 1: 75/25 train/test (Interpolation) >>> X_train, X_test, y_train, y_test = train_test_split(concrete[features], concrete[target], train_size=0.75, random_state=100) >>> evaluate_models(X_train, X_test, y_train, y_test) >>> # Ridge RMSE: 112.4 >>> # HistGradientBoostingRegressor RMSE: 26.33 >>> # lrboost RMSE: 25.06

>>> # Scenario 2: 50/50 train/test (Interpolation) >>> X_train, X_test, y_train, y_test = train_test_split(concrete[features], concrete[target], train_size=0.50, random_state=100) >>> evaluate_models(X_train, X_test, y_train, y_test) >>> # Ridge RMSE: 107.6 >>> # HistGradientBoostingRegressor RMSE: 26.6 >>> # lrboost RMSE: 23.55

>>> # Scenario 3: Training: CCS > 25, Testing: CCS <= 25 (Extrapolation) >>> train = concrete.loc[concrete['ccs'] > 25] >>> test = concrete.loc[concrete['ccs'] <= 25] >>> X_train = train[features] >>> y_train = train[target] >>> X_test = train[features] >>> y_test = train[target] >>> evaluate_models(X_train, X_test, y_train, y_test) >>> # Ridge RMSE: 89.26 >>> # HistGradientBoostingRegressor RMSE: 4.21 >>> # lrboost RMSE: 3.7

With zero tuning of either the lrboost internal GBDT fit to the residual or the “standard” GBDT, lrboost performs well.